January 24, 2021

QBID + NIIT: Income Management and Opportunities for Small Business S-Corp Owners

Financial adviser Tom Bodin provides four income management strategies to help business owners limit lifetime taxes as much as possible.

Starting in 2022, there may be two significant income thresholds facing S-Corp business owners: the Qualified Business Income Deduction (QBID) and the proposed Net Investment Income Tax (NIIT) found in the Build Back Better legislation. The challenge, then, is to identify strategies to maintain the tax benefit of the S-Corp entity without limiting business profitability, recognize applicable income thresholds, and apply a toolset to show an effective approach to minimizing taxes given the above thresholds.

To that end, let’s explore some approaches to managing income and engineering modified adjusted gross income (MAGI) for an S-Corp small business owner. Specifically, we’ll look at a Specified Service Business as it applies to the QBID. This designation will apply to medical, dental, legal, financial, accounting firms, and others.

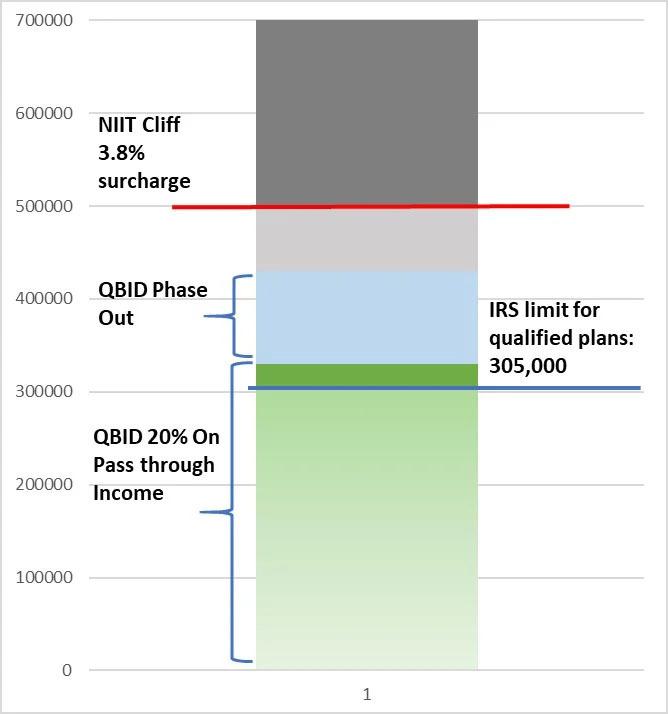

With this designation, the availability of the QBID phases out between $329,800 and $429,800 for the 2021 tax year for married taxpayers filing jointly, and between $164,900 and $214,900 for single filers. The QBID provides for a 20% reduction in pass-through income for tax purposes. With the current language in the Build Back Better legislation, the NIIT surcharge of 3.8% will begin to apply to pass-through income (the S-Corp profits) once income exceeds $500,000 for married taxpayers filing jointly or $400,000 for single filers.

When we look at income management, we are looking at two important aspects: how income is recognized and how much is taxed. Regarding the latter, qualified retirement plans are an important tool to engineer taxable income. For many Specified Service Business owners, combining a 401(k) with a Cash Balance plan can create significant flexibility to engineer taxable income. (Caveat: The rules around Cash Balance plans are complicated, so adopt them with caution.) This combination of a defined contribution plan and a defined benefit plan is generally referred to as “paired plan design.”

Let’s look at a scenario for an S-Corp business owner who is trying to manage $750,000 of business profitability. Within certain limits, the business owner can choose what level of W-2 income they recognize. The IRS requires an officer of a corporation to recognize a “reasonable salary,” which leaves room for interpretation. To avoid any issues with the IRS, don’t get cute on the low end of a “reasonable” salary range. Conversely, for qualified plan testing in 2022, the maximum salary taken into consideration is $305,000. This is the 401(a)(17) annual compensation limit. Recognizing W-2 income beyond this level will likely incur employer-related taxes without providing additional benefits to the business owner.

For purposes of tax mitigation and qualified plan optimization, the tradeoff of W-2 income to passthrough income is a planning opportunity. The greater the W-2 income, the greater the differential between Highly Compensated Employee (HCE) earnings and Non-Highly Compensated Employee (NHCE) earnings. And all else equal, the greater this differential, then the greater the allocation of employer-funded contributions to the business owner and/or other specific individuals will be. More passthrough income means that the S-Corp owner can recognize a higher QBID, so long as they are not phased out, and lower their employer tax.

Based on the above, and again assuming our hypothetical business owner gives us $750,000 in business income to work with, there is flexibility (within reason) on W-2 income to recognize, as well as two qualified plans to potentially utilize. Let’s walk through a couple of scenarios. Each tests certain planning solutions and assumes the business owner is married and filing jointly.

Scenario 1: Create no strategic plan. Recognize the 401(a)(17) limit W-2 income of $305,000 and recognize the remaining $445,000 in pass-through income. The business owner phases out of QBID, would recognize NIIT if the provision is passed, and creeps into the 37% tax bracket.

Scenario 2: The business owner focuses on savings goals and meeting qualified plan obligations but does not delve into strategic use of qualified plans or income recognition strategies. Our business owner recognizes the 401(a)(17) limit W-2 income of $305,000 to maximize plan allocation, recognizes $195,001 in pass-through income, and funds their paired plan arrangement to $249,999, hypothetically satisfying their 401(k) obligations and funding a Cash Balance plan’s accrued benefits. While earning substantial savings, the business owner still recognizes $500,001 in income, allowing them to avoid the proposed NIIT but phasing them out of QBID. This strategy avoids the 37% marginal bracket and lands the business owner squarely in the 35% tax bracket. This scenario would owe an estimated $123,355 in federal tax.

Scenario 3: Focus on driving income into a range that will fully avoid the proposed NIIT and capture a portion of QBID. The business owner continues to recognize the 401(a)(17) limit on W-2 income at $305,000, recognizes $95,000 in pass-through income, and funds their paired plan with the $305,000 of remaining profitability. With total income of $400,000, this strategy captures a QBID of $12,540 and holds income to the 32% marginal tax bracket. This scenario would owe an estimated $80,435 in federal tax.

Scenario 4: This scenario puts all the tools at the business owner’s disposal to work by driving income into a range that avoids NIIT and fully captures QBID. It also goes a step further and explores pulling off the 401(a)(17) limit to maximize passthrough income. In taking this step, work closely with your plan’s third-party administrator (TPA) to understand how lower income will affect your plan allocations and to find a sweet spot for W-2 income that offers the right mix of allocation benefits for the business owner and staff contributions to profit-sharing funds. When exploring this type of income recognition strategy, it is appropriate to account for the tax benefits from Qualified Business Deductions and from limiting employer taxes on pass-through income. This last scenario tests $200,000 in W-2 income and $129,800 in pass-through income. The remaining $420,200 of profit went to the paired qualified plans. This created taxable income of $329,800, allowing the business owner to capture all the QBID on the $129,800 in pass-through income. With the additional tax savings and deductions, the estimated income with this strategy places the taxpayer in the 24% marginal bracket with an effective rate of 16%. This scenario would owe an estimated $55,100 in federal tax.

Being able to affect these strategies is heavily reliant on an understanding of your living expenses. While you want to optimize opportunities for tax mitigation, you also want to be sure you’re not so aggressive in using those strategies that you are unable to support the lifestyle you are working so hard to enjoy.

Once you understand your desired and standard lifestyle expenses, explore a qualified plan design that can accommodate significant contributions. As mentioned, this generally can be accomplished through paired plan design.

The last element of this approach involves income recognition strategies. The allocation of profit-sharing and cash balance benefits are primarily factors of wage and age differentials. Recognizing a maximum 401(a)(17) W-2 salary (again, $305,000 in 2022) will provide the maximum allocation to the business owner relative to staff, but depending on certain factors, opting for the maximum income limit may miss a more refined strategy. Factors that may affect this decision include:

- Earnings differentials between owner and staff

- Age differentials between owner and staff

- Number and inclusion of higher-compensated employees

- Appropriate utilization of owner family members as employees (will default as HCE regardless of income based on relationship status)

Implementing an income management strategy cannot be done in a vacuum. Aggressive funding will need to be managed around lifetime plan limits as well as a repositioning strategy during the black-out period (the time between business ownership and required minimum distribution age). And, as always, the goal should be to limit lifetime taxes.

The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth®. This article is for general information and educational purposes only and is not intended to serve as specific financial, accounting, legal, or tax advice. Individuals should speak with qualified professionals based upon their individual circumstances. The analysis contained in this article may be based upon third-party information and may become outdated or otherwise superseded without notice. Third-party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, confirmed the accuracy, or determined the adequacy of this article. The scenarios above are hypothetical and do not reflect an actual client experience. Estimated federal tax amounts for each of the four hypothetical scenarios explored in this article were calculated using Holistiplan tax planning software. R-22-3123

© 2021 Buckingham Strategic Wealth®

This commentary originally appeared January 24, 2021 on thestreet.com

Category

Business OwnershipContent Topics

About the Author

Thomas Bodin

Practice Integration Advisor