March 13, 2023

The Right Time to Buy? How to Factor in Higher Mortgage Rates

No matter what happens in the market, a home purchase is often as much of an emotional decision as it is a financial one.

Recent trends in the housing market have prompted many potential homebuyers to ask: Is now a good time? In the past year, mortgage rates have not only doubled, but they also did so at a time when housing prices had reached historical highs. This combination potentially impacts the home purchasing decisions of millions of Americans. Here’s what to consider when deciding if you are ready to become a homeowner this year.

A Decade of Favorable Rates May be Coming to an End

If you purchased a home over the past two decades, you likely locked in a favorable rate. This is especially true in the years following the 2008 financial crisis and accompanying housing market collapse:

- In May 2013, the average 30-year fixed rate was 3.35%. For most years until 2019, rates fluctuated in the 3% to 4% range, rarely going above 4%. It was only in 2019 when they briefly spiked to over 5%.

- Then, because of pandemic-driven interest rate declines, mortgage rates fell even lower, to an average of 2.68% in December 2020.

- In 2022, however, things changed. Mostly because of factors tied to the pandemic, rates shot up between January and October. In that short 10 months, the average 30-year fixed rate went from 3.22% to 7.08%. It took less than a year for rates to fluctuate more than we’ve seen in decades.

Historical context puts today’s rates in perspective

Think mortgage rates seem high now? When looking at the last decade, or even the early 2000s when they averaged 5% to 6%, sure, they’ve increased. But when viewed from a broader historical perspective, a 7% mortgage rate begins to look much better.

Consider that mortgage rates in the early 1990s were nearly 10%. Or, how about this? In 1981, you may have been signing your name to a contract where you agreed to pay back a mortgage loan with a whopping 18% interest rate.

How rates move from here, and how quickly they do so, is still a matter of debate. But inflation appears to be stabilizing, which has allowed the Federal Reserve to slow the speed at which it increases rates. Still, for new buyers, higher interest rates will have an impact on their budgets and monthly loan payments.

Impact of Mortgage Rates on Payments

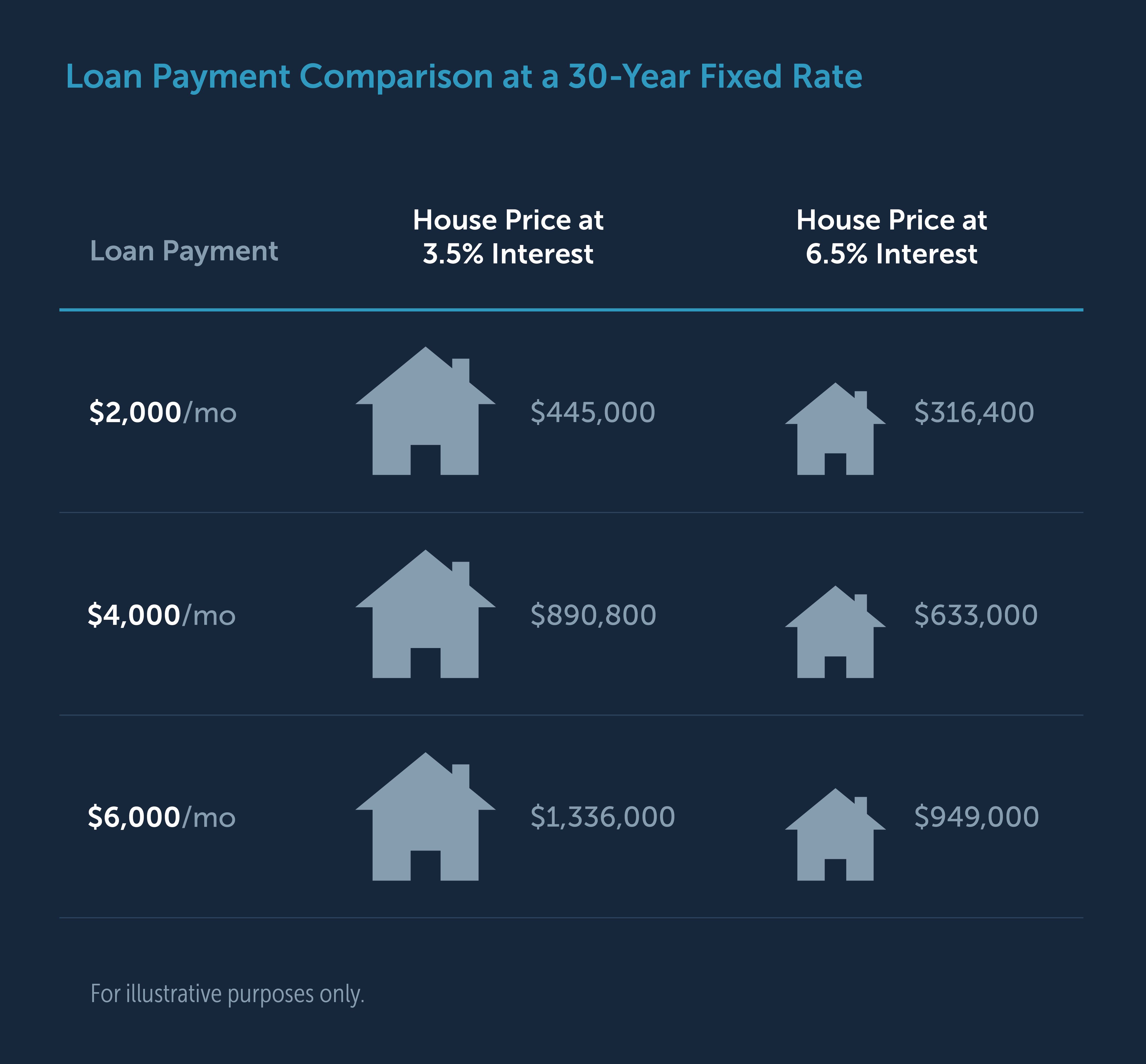

When planning for a home purchase, one of the biggest factors buyers tend to consider is “the amount of house” they can get for the money. While the total cost of a house is an important factor, often buyers are more concerned with what they can afford on a monthly basis.

When budgeting using a specific monthly payment, a higher interest rate eats away at the price you can spend on a home because you’ll need to allocate more money each month toward interest, rather than the principal loan payment. The chart below illustrates the impact.

Clearly, higher rates mean potential homebuyers might not be able to afford the same house they could have a year ago. However, for those in this situation, there may still be some options to secure a lower rate.

Opportunities for a Lower Mortgage Rate

- Shorter Duration Loans: Mortgage loans with shorter durations, such as 15 or 20 years, generally offer lower rates than the more traditional 30-year mortgage. This might be a good option for a buyer who has a larger budget and wants to pay off their mortgage quicker. However, they aren’t usually a great option for those looking to get the most house they can for a certain monthly payment. That’s because even though the rate is reduced, the monthly loan payment will generally increase significantly because the principal portion of the mortgage is compressed into fewer payments.

- Adjustable-Rate Mortgages (ARMs): ARMs also generally offer lower initial interest rates for a specified period. But, in an uncertain rate environment, ARMs can be risky. When the initial rate period expires, the new rate following the adjustment could be much higher.

- Compare: Not all lenders offer the same rates. Shop around. An independent financial advisor can also help you compare lenders, rates, terms and other factors to help you find the right loan option for you and your family.

- Mortgage Discount Points: Sometimes, you’re able to pay a fee upfront to lower your mortgage rate over the life of your loan. This type of fee is known as a “mortgage point.” If you’re planning to live in your new home for a long time, purchasing mortgage points could reduce your interest rate and long-term costs. Since you have to pay an upfront fee, though, there is a breakeven point to make the cost worthwhile. You’ll need to stay in the home long enough so that the amount you save in interest outweighs the cost of the points.

- Credit Score: If you will be in the market to buy a home in the future and do not have a favorable credit score, it is in your interest to look at ways to improve it. Small changes in your score could have cost-saving benefits when shopping for an interest rate.

- Down Payment: The amount you put toward your down payment may reduce your interest rate. Also, a higher down payment will lower the principal loan to be paid as well as the associated overall interest.

Mortgage rates aren’t the end of the story, however. There’s another side to the equation: home prices.

Predicting Housing Prices is a Tough Task

Typically, when interest rates rise, housing prices are expected to go down because the housing stock rises and the market becomes less competitive. This means that your dream home could still be in reach, even with higher mortgage rates. Unfortunately, there is no clear consensus about where things are headed.

Although housing prices have leveled off, or even declined in parts of the country, the recent increase in mortgage rates has not affected prices as much as many expected. Easing inflation and lack of inventory may mean that prices don’t decline as much as they have in past high interest rate environments. The good news is prices have at least stabilized, which could offer some comfort to homebuyers.

So, is now a good time to buy a house?

There are plenty of factors to consider beyond those in this article when deciding whether now is the right time for you to buy a house, such as where you are in your family life cycle. Current mortgage rates aren’t necessarily something that should outweigh all those other considerations.

Rates are higher, but not outside of historical norms. If they were to decline significantly, there would be opportunities to refinance at more favorable rates. And although home prices have increased since the pandemic, they have been stabilizing recently. If you are planning to live in your new home for 10 years or more, you likely won’t be affected by near-term price fluctuations.

In the end, buying a home is often as much of an emotional decision as it is a financial decision. Even if the current market isn’t considered optimal for buyers, it may still be the right time for you. If you're thinking about buying a new home, consider consulting with your Buckingham advisor who can help you evaluate your options.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Certain information is based on third-party data which may become outdated or otherwise superseded without notice. Third-party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. R-23-5139

Content Topics

About the Author

Matthew Nelson

Buckingham Advisor Resources Manager