February 02, 2021

Stocks, Risk, and Your Roth IRA

A great deal of attention often goes into deciding what a portfolio should own, especially when tailoring its allocation to specific retirement goals, risk tolerance, time horizon, and other individual factors.

But which types of accounts own which investments also deserves careful consideration, as an account’s tax treatment can affect the amount of overall portfolio risk. In other words, you can tilt the overall amount of risk in your portfolio higher or lower depending on whether you place certain investments in your taxable account, traditional IRA, or Roth IRA.

Uncle Sam Also Likes Your Investments to Grow

If you have ever received a 1099 for investment gains or losses or had to pay income taxes after taking a distribution from your traditional IRA, you’re well aware that Uncle Sam is your investment partner on such accounts. Just like you, Uncle Sam wants these accounts to grow, because bigger returns result in bigger balances and potentially more tax dollars. Losses on taxable accounts can be deducted, and as traditional IRA balances go down, it means fewer income-taxable dollars in the portfolio. But withdrawals from your Roth IRA are income-tax-free; at some point in the past, you’ve already paid income tax and essentially bought Uncle Sam out of the partnership. Uncle Sam doesn’t care whether your Roth value goes up or down anymore because there are no more tax dollars to be given or to be lost.

Taking Taxes into Account

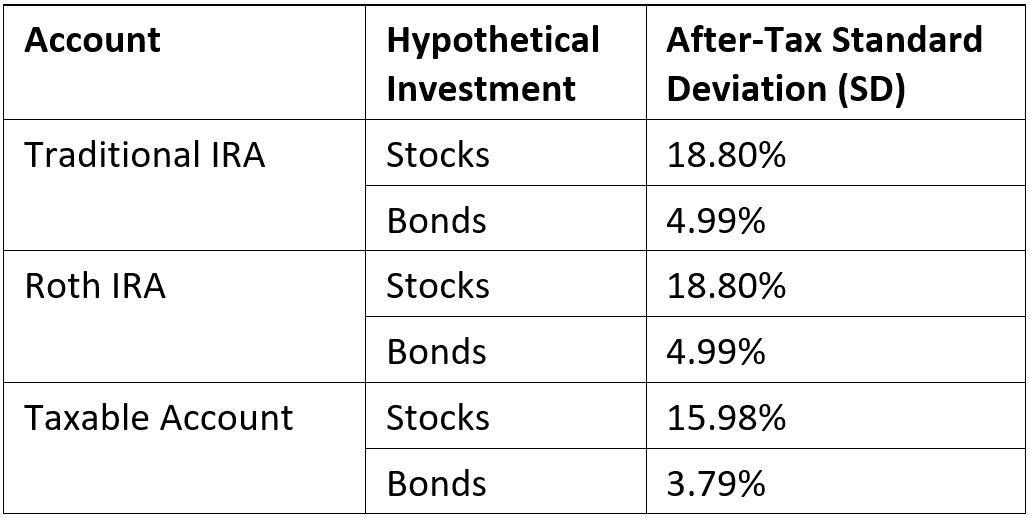

Many consider an account’s tax treatment when thinking about expected after-tax return, but fewer likely consider how an account’s tax treatment affects their expected risk. Let’s look at an example using a hypothetical stock allocation and a hypothetical bond allocation. We’ll assume a 24% federal income tax rate and a 15% long-term capital gains (LTCG) rate. Further, we’ll assume all of the return on stocks is taxed at LTCG rates each year and all bonds at income tax rates for the taxable account.

You’ll notice that after-tax standard deviations are lower when assets are held in the taxable account, as Uncle Sam participates in both the upside and downside risk of the investments there. Further, relative to holding the asset in a tax-advantaged account, stocks saw a greater reduction in standard deviation than bonds did. Traditional IRAs are tax-deferred, meaning you take all the risk until the “end,” when funds are taken out. In other words, Uncle Sam doesn’t participate in the risk of any individual investment, but rather just the balance being distributed. Given this, expected after-tax returns become important when deciding between placing an investment in your traditional IRA or your Roth, but not Uncle Sam’s participation in risk.

Let’s take our example one step further and assume a higher expected return on stocks than on bonds. All things equal, it may be obvious to consider buying stocks in your taxable account over your traditional IRA, as the portfolio would net a higher after-tax expected return while reducing after-tax stock risk. But when deciding whether to place our hypothetical stocks solely in the Roth or a taxable account, consider that stocks in the Roth account are inherently riskier because Uncle Sam doesn’t participate in the risk, even though the after-tax return of the Roth may be higher. Looking at this from a different angle, owning slightly more stock in the taxable account than otherwise would have been purchased in the Roth IRA could result in the same amount of overall, after-tax risk.

Impact

Periodically reviewing your portfolio to see if there are any opportunities to create efficiency by shifting where you own your investments is important. How would locating the investments you own today in one account versus another impact your portfolio’s overall risk? Is there an opportunity to potentially keep your portfolio’s overall after-tax risk the same, but increase expected after-tax returns by changing where you hold certain investments and exactly how much of them you own?

When deciding which investments should go into which account, think not only in terms of expected after-tax returns but also in terms of after-tax risk. Sharing risk with Uncle Sam means you could potentially take on more of it, knowing you’re in it together. Or, when risk isn’t the concern, maybe you don’t want the government as your investment partner.

This commentary originally appeared January 8 on thestreet.com.

The information presented here is for educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Individuals should seek advice from a qualified professional based on their individual circumstances. Information contained herein may be based upon third-party information and may become outdated or otherwise superseded at any time without notice. Third-party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth®.

By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. IRN-20-1614

© 2021 Buckingham Strategic Wealth®

Category

InvestingAbout the Author

Patrick Kuster

Wealth Advisor