October 17, 2022

Should You File for Social Security Early to Capture the Inflation Adjustment?

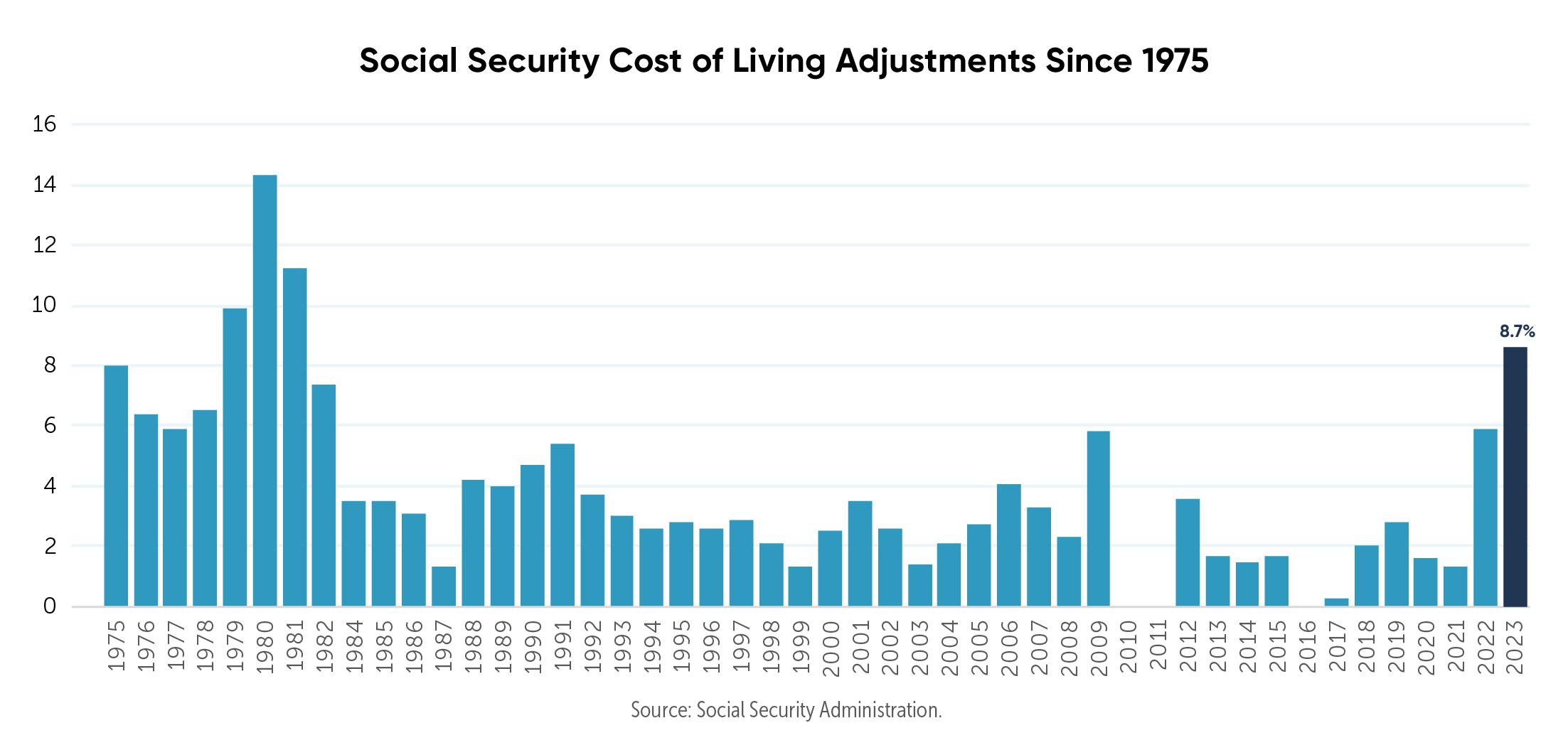

Social Security benefits will go up 8.7% in 2023, the largest adjustment in four decades. Here’s why you don’t need to rush to file to benefit from the increase.

With all the talk about inflation these days, you may have heard the news that the 2023 cost-of-living adjustment (COLA) for Social Security benefits is 8.7%, the largest in four decades. If you are approaching or over age 62 and haven’t filed for your retirement benefits, you may be wondering if you should file earlier than planned so you do not miss out on the increase.

The reality is that you do not need to file now to benefit from the COLA increase. Starting in the year you turn 62 any COLA will be calculated into your benefit amount, whether you choose to file that year or wait longer (you can file any year from age 62 up to 70).

What is the COLA?

In 1975, the Social Security Administration began adding annual increases to retirement benefits to keep up with rising costs based on the rate of inflation. If there is no inflation, there is no COLA. Although the COLA has been 0% three times, it has never been negative, even in periods of deflation. The COLA, however, does not only affect current benefits. It also applies to all future benefits and even the maximum taxable earnings on which wage earners pay into the system.

How is the COLA calculated?

The timing and methods for calculating COLA have changed over time. Since 1984, the Social Security Administration has based COLA on increases in the Consumer Price Index for Urban Wage Earners and Clerical Workers (or CPI-W), comparing the average CPI-W from the third quarter of the current year to that of the prior year.

What is the 2023 COLA?

The Social Security Administration announced on Oct. 13 that the 2023 COLA increase will be 8.7%, the highest increase since 1981. That means payments will go up by more than $140 per month, on average, starting in January.

If you currently receive benefits, you should receive your COLA notice via your online Social Security account before the end of December, and you will receive your increased benefit amount in January.

If you have not filed for benefits but are curious how the change will affect your payment, you can go to your online account and view your full retirement age benefit amount before the end of the year. Then you can check again in January to see the increase reflected.

Should I file now so I do not miss out on the COLA?

While everyone’s situation is different, generally there are good reasons to delay filing for your Social Security benefits, especially if you have other income sources you can rely on. For example, filing too early might permanently reduce your benefits, it may lead to adverse tax implications, or you may be subject to an earnings test that reduces your current benefits.

Many do not realize that Social Security is protected against inflation, one of the reasons Buckingham advisors view Social Security as a form of longevity insurance. And in fact, even for individuals who plan to file in the future, annual COLAs are still factored into their future benefits from the year they turn 62. So, you do not lose out on this benefit by waiting to file.

If you chose to file earlier than you would have under the assumption you might miss out on the increase, there may be options to consider. For example, you can get a one-time “do-over” by filing a request to withdrawal your application up to 12 months after filing. This will cancel your benefits so you can reapply later, but you will need to repay any benefits that you’ve received. Alternatively, if you are older than full retirement age (66 or 67, depending on your birth year), you can suspend your benefits so that they continue to grow at a rate of 8% per year up to age 70. If you suspend, however, any benefits that family members receive based on your benefit, such as a spousal benefit, will also be suspended. We would recommend consulting with your financial advisor as soon as possible to help determine the right course of action for you.

I’m already receiving benefits. Will the COLA be enough for me?

The short answer is it depends. Perhaps you have other financial resources and don’t have to rely as heavily on Social Security for all your income needs. Also, depending on your spending habits, you may not be as affected by the rate of inflation as others. Interestingly, the CPI-W used to determine the adjustment reflects inflation for a particular subset of workers (urban wage earners and clerical workers) who are paying into Social Security, not those who are retired and actually receiving benefits.

Each person’s situation and spending habits are different, so if you have concerns it may be helpful to review your plan with your advisor. If you are not currently working with one, we would love to help you. Please schedule a short phone call or virtual conversation with our Client Development team.

About the authors:

Steve Weiss, CFP® joined Buckingham Strategic Wealth in 2012 as a portfolio advisor. Today, as a wealth advisor, he assists clients with making important financial decisions. Prior to that, he was at the firm Enterprise Bank & Trust where he held such titles as trust operations specialist, paraplanner, and investment and planning specialist. He earned a bachelor’s degree in communication from the University of Michigan and is a CERTIFIED FINANCIAL PLANNERTM professional.

Jim Cornfeld, CFP® joined Buckingham Strategic Wealth in 2006. Prior to that, he was vice president and portfolio manager for First Bank Wealth Management Group. He spent 18 years with Mobil Oil Corporation in its marketing division, representing Mobil globally from its offices in Africa, Australia and New York. Jim is a CERTIFIED FINANCIAL PLANNERTM and chairs the firm’s Advanced Planning Committee.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party information which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Individuals should speak with a qualified financial professional based on their own circumstances. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth®. R-22-4562