November 21, 2022

Inherited an IRA? Here’s Why Planning Distributions Early Matters

If you’ve inherited an IRA recently, here’s what you need to know about planning distributions and keeping up with changing tax rules.

Those who have inherited an IRA since 2020 may be finding it a challenge to keep up with evolving account distribution requirements and IRS messaging. Distribution rules the IRS proposed earlier this year only added to the confusion. Below are some common questions that should be considered when planning for required minimum distributions (RMDs) and other withdrawals from an inherited IRA in 2023 and beyond.

Is it possible to spread IRA account distributions out over your lifetime?

Before 2020, when someone other than a spouse inherited an IRA, the beneficiary could spread the distributions and accompanying taxes out over their lifetime, which was often several decades or more. This was commonly referred to as a Stretch IRA. For most non-spouse beneficiaries, excluding eligible designated beneficiaries, the ability to stretch out distributions over time was eliminated with the passing of the Setting Every Community Up for Retirement Enhancement (SECURE) Act, which went into effect in 2020.

Because of the SECURE Act, most non-spouse beneficiaries who inherited a retirement account in 2020 or after became subject to the 10-year rule. This rule requires all funds to be distributed by the end of the 10th year following the death of the IRA owner.

Does the 10-year rule require annual IRA distributions or only by the end of the 10th year?

When the SECURE Act passed, it did not specify whether annual distributions would be needed within the 10-year period. So, most tax professionals assumed that a beneficiary could wait to withdraw all funds in the 10th year.

However, in February 2022, the IRS issued proposed regulations that said beneficiaries subject to the 10-year rule would also need to take annual RMDs if the deceased IRA owner had died on or after their required beginning date, which is April 1 of the year after the deceased IRA owner turned 72. That meant affected beneficiaries should have taken RMDs in 2021 and would need to again in 2022. Those beneficiaries who did not risked being subject to a 50% penalty on the funds that should have been distributed.

The proposed regulations caused confusion and concern for taxpayers, so the IRS issued Notice 2022-53 in October, which stated that all beneficiaries subject to the 10-year rule are exempt from taking RMDs for 2021 and 2022.

Will the IRS ultimately require annual IRA distributions for those subject to the 10-year rule?

The IRS notice in October did not address whether RMDs would be required in 2023 and beyond. The silence could be an indication that the IRS intends to follow the interpretation it laid out in its proposed regulations and require annual minimum distributions on inherited IRAs after 2022. Or the IRS could be planning to reverse course and eliminate annual RMDs altogether for beneficiaries of the 10-year rule. Ultimately, we’ll just have to wait and see.

Does it make sense to take voluntary distributions from an inherited IRA?

Even if you are not required to take an annual distribution from your account, if you are a beneficiary subject to the 10-year rule, you may want to consider taking a voluntary distribution. Spreading distributions out as much as possible during the 10-year window can help reduce the chance that larger distributions in future years create a bigger tax bill. This can happen if a large distribution in one year pushes the beneficiary into a higher tax bracket. It might also lead to the beneficiary being phased out of critical deductions or credits.

How might voluntary IRA distributions save on taxes in the long run?

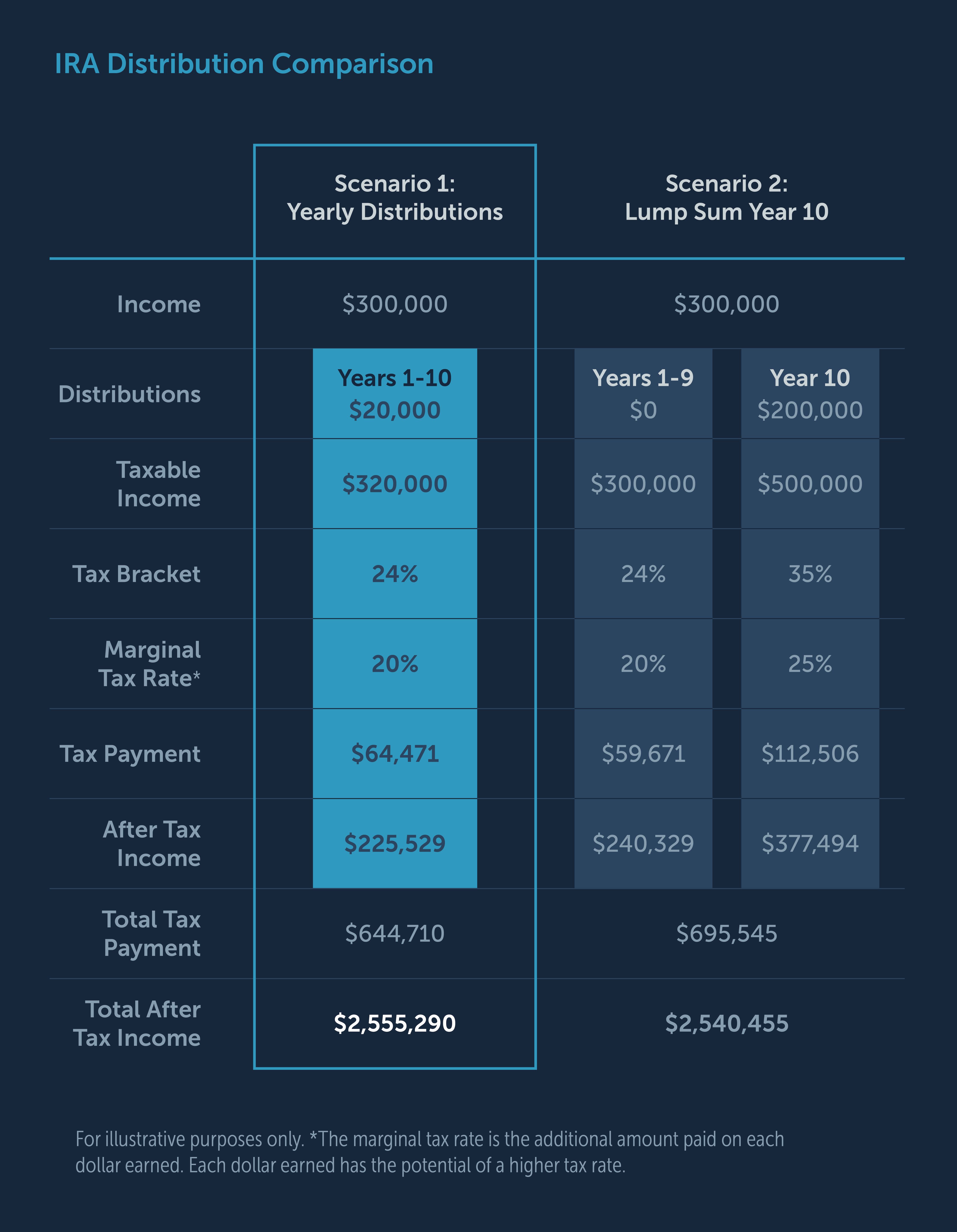

Let’s consider a married couple filing jointly who has taxable income of $300,000. For 2022, this places them in the 24% tax bracket, based on tax-year 2023 IRS inflation adjustments. They can earn an additional $40,100 of taxable income, for a total taxable income of $340,100, before worrying about being bumped into the 32% tax bracket. It would take an additional $131,900 of taxable income, for a total taxable income of $431,900, before they would find themselves in the 35% tax bracket.

Now, let’s assume one of them inherited an IRA with assets worth $200,000, and each year the account, their income and the tax bracket inflation adjustments remain constant. It would take roughly five years for the couple to deplete the account without being pushed into the next tax bracket. If they begin withdrawals immediately, they could take out $20,000 annually over the 10-year period. After that, they could be forced to take larger sums that would increase their bracket. The below chart illustrates how this would look.

In Scenario 1, the couple takes $20,000 from the IRA each year, while in Scenario 2, the couple takes all funds in the account in the 10th year. The result is that the couple in Scenario 2 pays roughly $15,000 more in total taxes because their income moved them into the 35% tax bracket in year 10.

The long-term advantages of planning IRA distributions

Although the above comparison is only hypothetical, as many uncontrollable factors will influence income, investments and tax brackets over time, it serves to demonstrate how proper planning helps prepare for the associated tax implications. If someone waits too long to take any distributions, they may be forced to take large sums just before the 10-year window closes, resulting in adverse tax consequences.

To minimize the impact of income taxes on your inheritance, the timing of your distributions should be coordinated with other anticipated income, deductions and credits as well as other tax attributes. The good news is that this is something your advisor can help with.

If you are not currently working with an advisor, we would love to help you. Please schedule a short phone call or virtual conversation with our Client Development team.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party information and may become outdated or otherwise superseded without notice. Third-party information is deemed reliable, but its accuracy and completeness cannot be guaranteed. Individuals should speak with a qualified tax and financial professional based on their own circumstances to determine if the above scenarios are applicable. R-22-4732

Category

Tax StrategiesContent Topics

About the Author

Matthew Nelson

Buckingham Advisor Resources Manager